Blog

Welcome and thanks for stopping by! My blog is filled with market updates and real estate info, but also Richmond area spots and favorites, fun stories and lots of recipes that I love (please try them!).

I love to share, and never gatekeep, so please bookmark my blog, check back often, and of course, don’t forget to subscribe to my newsletter!

Click each event below for more information. For a full calendar of events, click HERE. Friday Cheers (1st of the Season!) Richmond Flower Truck Floral Arrangement Workshop Lewis Ginter Spring Plant Sale 54th Annual Art in the Park Mother's Day Concert at Agecroft Hall 5k Family Fun Day at Crump Park Big Tent: Memorial Day Event Family Night Hike

Read more

This is without a doubt one of the best carrot cakes I've ever had, if I do say so myself. When I had Gourmet Delights, and my food rep came in one day with a delicious, but criminally expensive, carrot cake, I had to come up with something that was close so I didn't have to sell it for $5 per slice. (Hilarious that that seemed outrageous at the time.) This is what I came up with. Servings: 12 | Prep time: 25 minutes | Total Time: 1 hour Ingredients 2 cups sugar 1 cup vegetable oil 4 large eggs 3 cups grated carrot 1 teaspoon vanilla 1 teaspoon cinnamon 1/2 teaspoon ginger 2 1/2 cups flour 1 1/2 teaspoons baking powder 1 teaspoon baking soda 1/2 teaspoon salt 1/2 cup chopped pecans 1/2 cup raisins Frosting: 8 ounces cream cheese 5 tablespoons unsalted butter, room temperature 2 teaspoons vanilla 2 cups powdered sugar Directions Heat oven to 350. Combine sugar and oil in a bowl and beat until well combined. Add eggs, carrots, cinnamon, ginger, and vanilla. Beat until well mixed. Stir together flour, baking powder, baking soda, and salt in a medium bowl. Add dry mixture to liquids gradually, beating after each addition to ensure they are well combined. Stir in nuts and raisins. Pour mixture into 2 greased and floured (preferably also lined with parchment too) 8" round cake pans. Bake until toothpick inserted in center comes out clean. 35-40 minutes. Frost with cream cheese frosting. In medium bowl, beat together cream cheese, butter, and vanilla until just blended. Add powdered sugar, a bit at a time, until well blended. Taking care not to overbeat. Frost when cake is cooled.

Read more

Click each event below for more information, for a full calendar of events click HERE. Hardywood's Spring Artisan Market Spring Bloom Bar with Freckled Flower RVA Burlesque Festival The Big Bloom The Bizarre Bazaar 33rd Annual Spring Market Ukrop's Monument Avenue 10k April Fools Festival Scotchtown's 4th Annual Fiber Festival Dominion Energy Family Easter SCAN Totally 90s Bash

Read more

For a printable checklist, click HERE.

Read more

Let's take a look into how the changes to agent commissions are reshaping real estate transactions, impacting home buyers and sellers alike six months after going into effect, here in 2025. Have questions? Ready to talk real estate? Send me a message here or via Instagram at CindyBennettRealEstate.

Read more

As I type this, we've got just 2 weeks until my son heads to Japan for nearly 4.5 months. He's super excited, and I'm excited for him. (Just a little bit of mom worry.) But he, like me, is quite a foodie, so it wouldn't be us if we didn't have a list to tackle in terms of spots to dine or takeout before he heads to the land of fantastic, but totally different, food. Starting out with the easy picks, because they're the "always" picks. We both love a great sandwich, so we'll definitely be dining or getting take out from... Stuffy's There's no question Stuffy's is a Richmond institution. My go to? The Great Garden on wheat pita, heated, with everything but mayo (that means it's an all veg dream, cheese, mushrooms, onions, green peppers, black olives, spinach, cucumbers, tomatoes, sprouts, oil, vinegar, s & p, and oregano. His? The Max, or Stuffy's Star (Classic Italian) Polpetti It's hard to choose the perfect one from Polpetti, because I've never had a bad sandwich there, and some days I'm feeling one or the other, but the go to is nearly always The Balboa- shaved Italian roast pork, broccoli raab, sharp provolone, with long hot peppers. Or The Caputo- roasted red peppers, arugula, fresh mozzarella, & balsamic glaze if I'm feeling like something more light. One thing's for sure, we're always going to share, and we're always getting at least one chicken cutlet sandwich- probably The OG- chicken cutlet, sharp provolone, broccoli raab, and long hot peppers. Abuelita's Funnily enough, almost every time we go here, my Mom is with us, and that is a testament to how they appeal to everyone! Their menu changes every day, but I've never had anything bad there. This is not your run of the mill Mexican. Their main option is Guisos (stews) and they always have a great variety. Served with beans, rice, and warm tortillas, they are delicious every time. They also do tamales, quesaberria tacos. (Oh, and a killer flan and tres leches as well.) The Oh So RVA picks that he always hits when he's in town... Mekong Fun fact- did you know my kid spent a focused couple of years trying everything on their menu, in order? We've been die hards since he was just starting solid foods, so this is definitely on the list. My go to? Always the Rice Noodle Salad with tofu and spring roll. It's light, but not too light, and with fresh vegetables, rice noodles, a little peanut, and delicious fish sauce, it's just the perfect bowl of the perfect bites. His go to? It depends on the day, his mood, and where his is on the menu! Thai Diner This has been an OG favorite since my kid was little bitty. He is an "American Hot" person, though he's dabbled in the world of Thai hot. Me? I'm a wimp and stick to mild or medium. Our picks here- Drunken Noodles with Chicken or Thai Fried Rice with Beef. So dang good. 8 1/2 Another lifelong favorite, we've got a "go to" order here as well. I'm always in the mood for their Eggplant Parm, with a side of spaghetti marinara, a spaghetti carbonara, or an order of penne with sausage, ricotta, and broccoletti. Never hurts to have leftovers, right? Wood and Iron Gameday You can't leave America for months without hitting a sports bar, can you? (I'm pretty sure that's a law) We'll definitely be hitting Wood and Iron one evening soon. Me for the Crispy Chicken Salad (pro tip- get a full sized, but just ask for a takeout container when you order, and you've got lunch for tomorrow), and him for the Cheese Steak Egg Rolls and an order of wings. Secret Sandwich Society Four words. Loaded Pimento Cheese Fries. Is that the only thing on the list? No. Could it be? Yes. I'm not even a "loaded" whatever sort of fan, but these are amazing. He's more a Roosevelt guy, roast beef, bacon, horseradish mayo, white cheddar, lettuce, tomato & red onions all on a toasted baguette and I love the Lafayette- fried chicken breast, ham, swiss, blue cheese spread & honey mustard on a toasted potato roll. Galley Go To One of our first picks for pizza, ever since they opened. Always on the order? Grape and Gorgonzola (Those roasted grapes with the sharp taste of the gorgonzola? Never fails.) We also always do the Sweet Hot, which features pepperoni, Calabrian peppers, and a drizzle of honey. You can't go wrong with either, but we can never choose between the two, so there you go. I'm full just thinking about all of this. (And yes, I'm cooking too!) What would be on your list??

Read more

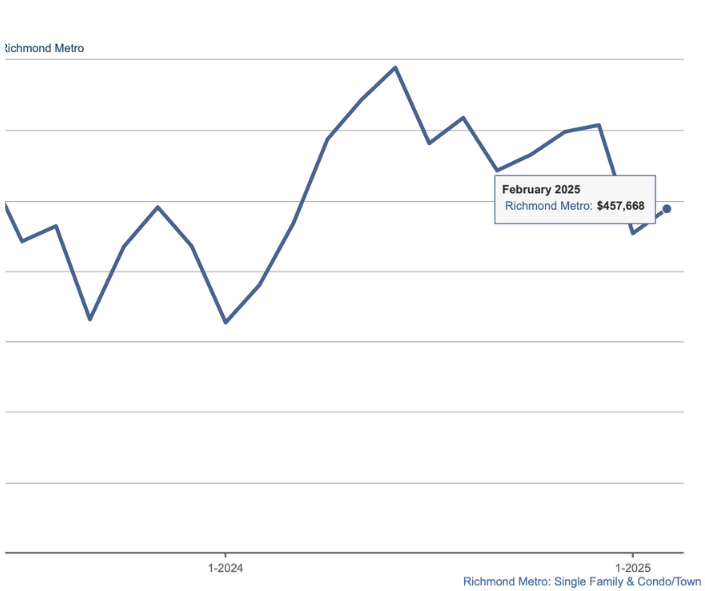

Market updates are a bit like tapping the mic with an "is this thing on?" People say they want them, but I always wonder how much they actually get read. So if you're reading this, please let me know! March 20 heralds the first day of Spring, and I for one couldn't be more excited. But if we're talking about the market, it really has felt like spring for a while now! Here's a little bit of data to give you a snapshot of the overall market in the Richmond Metro. The average sales price in the Richmond Metro in February was $476,907. That's a bit lower than the prices in December, but a bounce back from a lower January price of $469,296, and it looks like it's back on the upward trend. If you've followed me for a little bit, you've probably heard me talk about the months supply, and how at a balanced market, we'd have about 6 months of inventory. It's been a while since we've been there, and for the last 2 months, we're holding strong at 1.3 months of inventory. A good distance from balance. This data tracks in what I've seen in the last couple of weeks, as well. Lower inventory means you may need to compete to get that home you love, because there are simply more buyers than there are great houses. Sometimes that means you have to pay more, but sometimes it just means having as much info as you need to craft an offer that will be the most appealing to the seller. Every situation is a little different, so there really is no one size all formula here. If you're selling, lower inventory means you have more eyeballs on your house, usually more showings, and (in many cases) more offers. Yes. You only need one offer, but the nice thing about multiple offers for you as a seller is that when people are competing, you're less likely to have to deal with a lot of inspection issues, you usually get more money, and you are more in the driver's seat with the entire transaction. We're seeing lots of multiple offer situations, although the market is quite price sensitive. What does that mean? You can't just thrown any home on the market, at any price, and think it's going to sell. The homes that are not "market ready" are still sitting on the market, and generally not getting multiple offers. Having your home ready makes a huge difference, as does pricing it well. Price it too high, and it just might sit there as well. There are definitely neighborhoods and areas that are more popular, and others where things are not quite as "wild." Knowing which one you're in, or looking in, can make a huge difference. I'd love to talk to you about the area you're in (or want to be in) and help you determine the best strategy to get you where you want to be. What are your market questions? Reach out!

Read more

Unlock the secret to choosing the right realtor with what I believe is the "game-changing" opening question for every interview. Ready to get started or just curious? Send me a message here on my website or send me an email at [email protected].

Read more

It's March, and that means St. Patrick's Day is almost here! In my family, that doesn't mean beer as much as it always, always, always, means plentiful corned beef and cabbage. (In fact, whenever my mom finds a good deal on corned beef- usually this time of year- she'll buy 3 or 4 and freeze them for later) If you love it as much as we do (impossible!), here's a great recipe using the Instant Pot so you can set it, forget it, and don't spend all day in the kitchen. Ingredients 1 3-pound corned beef brisket, plus pickling spice packet or 1 1/2 tablespoons pickling spice 1 medium onion, sliced 3 cloves garlic, chopped 1 (14.9 oz) Guinness beer 1 cup beef broth 1 pound new potatoes 3 large carrots, cut into 3-inch pieces 1 head Savoy cabbage, cut into 2-inch wedges Kosher salt and freshly ground pepper, to taste 2 tablespoons whole grain mustard Directions Rinse brisket with cold water and thoroughly pat dry. Place onion, garlic and pickling spice into a 6 qt Instant Pot. Gently place brisket on top of the onion mixture. Top with beer and beef broth. Select manual setting; adjust pressure to high, and set time for 85 minutes. When finished cooking, quick-release pressure according to manufacturer’s directions. Remove brisket from the Instant Pot; wrap in foil and keep in a warm oven. Remove and discard onion mixture, reserving 1 1/2 cups cooking liquid in the Instant Pot. Stir in potatoes and carrots; top with cabbage. Season with salt and pepper, to taste. Select manual setting; adjust pressure to high, and set time for 4 minutes. When finished cooking, quick-release pressure according to manufacturer’s directions. Thinly slice corned beef against the grain and serve with potatoes, carrots and cabbage Serve mustard on the side, if desired. Try to save a bit for some hash or a sandwich the next day!

Read more

Click each event below for more information, for a full calendar of events click HERE. Do Portugal Circus Pours & Pasties Burlesque and Variety Show St. Patrick's Day Charcuterie Workshop RVA Brick Day 2025 Virginia Derby Shamrock the Block The Irish Festival Pretend Again: A Grown-Up Night at the Museum Richmond SPCA Dog Jog, 5k, and Block Party The Wizard of Oz on Ice

Read more